Starting a business is exciting, but growing a business requires money. Whether you are launching a startup, opening a second branch, buying equipment, hiring employees, or simply managing day-to-day operations, access to capital can determine whether your business succeeds or struggles.

This is why business loans remain one of the most important financing tools for entrepreneurs and companies in 2026.

The problem is that many business owners either:

- Get rejected because they are unprepared

- Accept expensive loans with high interest rates

- Borrow more than they can realistically repay

- Choose the wrong financing option for their business needs

A business loan should help your company grow — not create long-term financial pressure.

That’s why understanding how commercial financing works is essential before applying for any loan.

This complete business loan guide explains everything you need to know about commercial financing in 2026, including business loan types, approval requirements, interest rates, secured vs unsecured financing, online lenders, startup funding, and smart borrowing strategies to help you secure funding more successfully.

Whether you are a first-time entrepreneur, small business owner, freelancer, or growing company, this guide will help you make more informed financing decisions.

What Is a Business Loan?

A business loan is a type of financing specifically designed for business purposes.

Unlike personal loans, business loans are intended to support commercial activities such as:

- Business expansion

- Inventory purchase

- Equipment financing

- Working capital

- Hiring employees

- Marketing campaigns

- Cash flow management

- Office setup

- Technology upgrades

The lender provides funds to the business, and the borrower repays the amount over time along with interest or financing charges.

Business loans may be offered by:

- Banks

- Islamic banks

- Microfinance institutions

- Online lenders

- Government-backed programs

- Fintech financing companies

Key Features of Business Loans

Business financing usually includes several important features.

Higher Loan Amounts

Business loans generally offer larger financing amounts compared to personal loans.

Flexible Repayment Terms

Repayment periods vary depending on the loan type and business needs.

Secured or Unsecured Options

Some loans require collateral, while others do not.

Variable Interest Rates

Rates depend on factors such as:

- Credit profile

- Revenue

- Industry risk

- Business age

- Loan amount

Why Businesses Need Loans

Businesses often require financing at different growth stages.

A loan can provide the capital needed to scale operations and improve profitability.

1. Business Expansion

Growing businesses may need funding to:

- Open new locations

- Enter new markets

- Increase production

- Launch new products

Expansion often requires significant investment before profits increase.

2. Inventory Purchase

Retail and product-based businesses frequently need capital to purchase inventory.

This is especially important during:

- Seasonal demand

- Holiday sales

- Large customer orders

Inventory financing helps businesses avoid stock shortages.

3. Cash Flow Management

Even profitable businesses can experience temporary cash flow shortages.

Business loans can help cover:

- Salaries

- Rent

- Supplier payments

- Utilities

- Operational expenses

Working capital financing is commonly used for this purpose.

4. Equipment and Technology Upgrades

Modern equipment improves productivity and efficiency.

Businesses often borrow money to purchase:

- Machinery

- Vehicles

- Computers

- Manufacturing tools

- Restaurant equipment

- Medical devices

Upgrading equipment can improve competitiveness and long-term profitability.

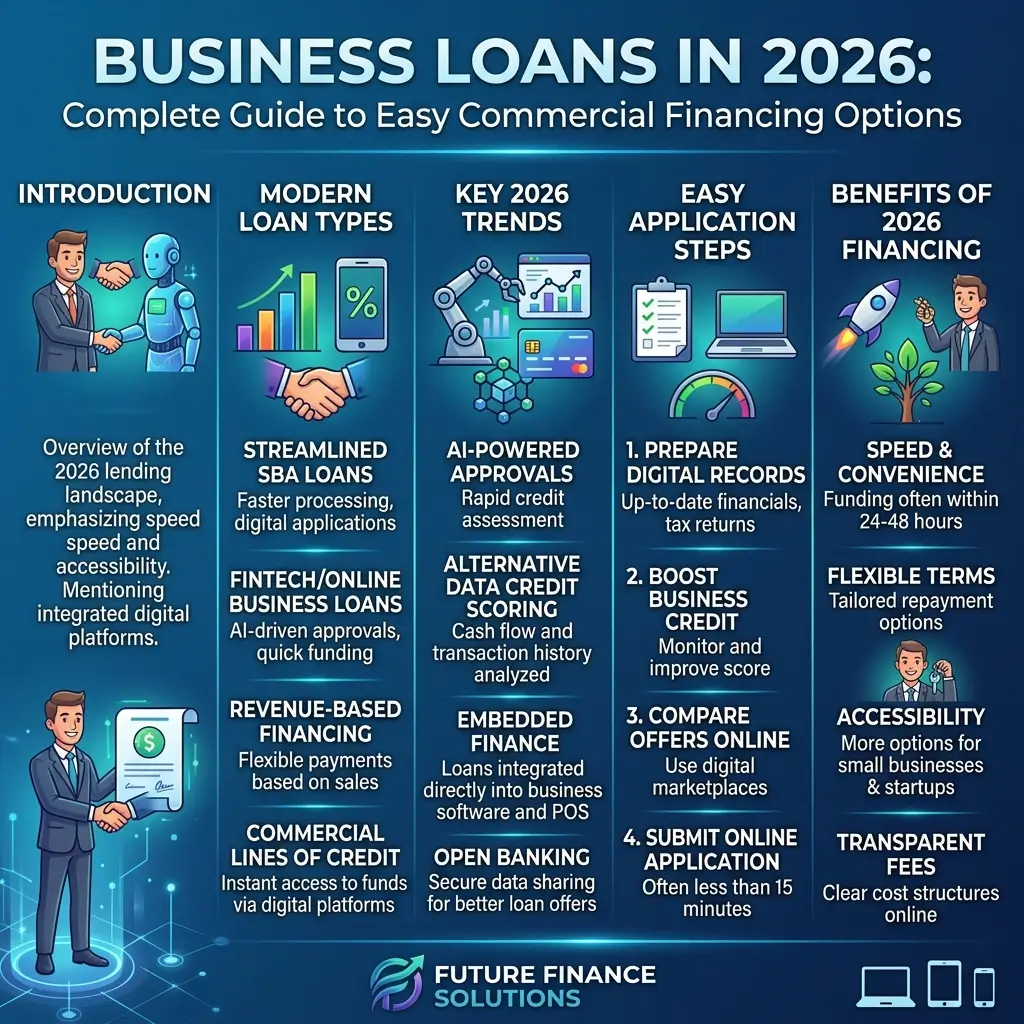

Types of Business Loans in 2026

Different businesses require different financing solutions.

Understanding the available loan types helps you choose the right option.

1. Term Loans

A term loan provides a fixed amount of money repaid over a specific period.

Features

- Fixed repayment schedule

- Monthly installments

- Predictable payments

Best For

- Expansion projects

- Long-term investments

- Large purchases

Term loans are among the most common commercial financing options.

2. Working Capital Loans

Working capital loans are short-term loans used for daily business operations.

Common Uses

- Payroll

- Inventory

- Utility bills

- Rent

- Supplier payments

Best For

Businesses needing temporary liquidity support.

Working capital financing helps businesses maintain smooth operations during slower cash flow periods.

3. Equipment Financing

Equipment loans are designed specifically for purchasing machinery or business equipment.

In many cases, the equipment itself serves as collateral.

Benefits

- Easier approval

- Lower interest rates

- Preserves business cash flow

Best For

Businesses needing expensive equipment upgrades.

4. Business Line of Credit

A business line of credit works similarly to a credit card.

The lender approves a borrowing limit, and the business can access funds when needed.

Key Advantage

You only pay interest on the amount you actually use.

Best For

- Cash flow flexibility

- Emergency expenses

- Seasonal businesses

A line of credit can provide ongoing financial support without taking a large lump-sum loan.

5. SBA or Government-Backed Loans

In some countries, governments support small business financing programs.

These loans may offer:

- Lower interest rates

- Easier repayment terms

- Partial government guarantees

Best For

- Small businesses

- Startups

- First-time entrepreneurs

Government-backed financing often helps businesses that struggle to qualify for traditional loans.

Secured vs Unsecured Business Loans

Business loans generally fall into two major categories.

Secured Business Loans

Secured loans require collateral such as:

- Property

- Equipment

- Inventory

- Vehicles

Advantages

- Lower interest rates

- Larger loan amounts

- Easier approval

Disadvantages

- Risk of losing collateral

- More documentation

Secured loans are common for established businesses.

Unsecured Business Loans

Unsecured loans do not require collateral.

Advantages

- No asset risk

- Faster approval

- Easier for small financing needs

Disadvantages

- Higher interest rates

- Smaller loan amounts

- Stricter credit requirements

Unsecured financing is often used by startups or businesses without major assets.

How to Get a Business Loan Easily

Business loan approval depends heavily on preparation.

Many businesses are rejected because they fail to present strong financial information.

Here’s how to improve your chances.

Step 1: Prepare a Strong Business Plan

A business plan shows lenders how your business operates and how you plan to repay the loan.

Your business plan should include:

- Business model

- Revenue projections

- Growth strategy

- Market analysis

- Financial forecasts

- Loan purpose

A well-prepared plan increases lender confidence.

Step 2: Check Your Credit Profile

Both personal and business credit history matter.

Lenders often review:

- Payment history

- Existing debt

- Credit utilization

- Financial discipline

Improving your credit score before applying can help you secure better rates.

Step 3: Choose the Right Lender

Different lenders serve different types of borrowers.

Options include:

- Traditional banks

- Islamic banks

- Online lenders

- Microfinance institutions

- Fintech financing companies

Compare multiple options before applying.

Step 4: Gather Required Documents

Being organized speeds up approval and improves credibility.

Commonly required documents include:

- Business registration certificate

- Financial statements

- Bank statements

- Tax returns

- Owner identification

- Profit and loss reports

Incomplete documentation often delays approval.

Factors That Affect Business Loan Approval

Lenders evaluate several factors before approving financing.

1. Credit Score

A strong credit score improves approval chances and lowers interest rates.

2. Business Age

Older businesses are usually considered less risky.

Startups often face stricter approval requirements.

3. Revenue and Profitability

Consistent income shows that the business can repay the loan.

Stable cash flow is one of the strongest approval factors.

4. Collateral

Providing collateral reduces lender risk and improves financing terms.

5. Industry Type

Some industries are considered higher risk than others.

For example:

- Restaurants

- Construction

- Startups

- Seasonal businesses

may face stricter lending conditions.

Business Loan Interest Rates in 2026

Business loan interest rates vary significantly depending on the borrower profile and financing type.

Typical ranges include:

| Business Profile | Typical Interest Rate |

|---|---|

| Low-risk businesses | 8% – 15% |

| Medium-risk businesses | 15% – 25% |

| High-risk startups | 25% – 40%+ |

Rates depend on:

- Creditworthiness

- Business performance

- Loan size

- Loan type

- Market conditions

- Collateral

Newer or riskier businesses usually pay higher rates.

How to Reduce Your Business Loan Interest Rate

Lower rates can save businesses a substantial amount over time.

Here are effective ways to improve financing terms.

1. Improve Your Credit Score

Pay debts on time and maintain strong financial discipline.

A better score often means lower interest rates.

2. Offer Collateral

Secured loans usually carry lower rates because the lender has reduced risk.

3. Show Strong Cash Flow

Lenders trust businesses with stable revenue and healthy financial records.

4. Compare Multiple Offers

Never accept the first offer without comparison.

Different lenders may provide significantly different terms.

5. Negotiate Loan Terms

Many borrowers do not negotiate — but lenders often have flexibility.

Strong businesses may qualify for:

- Lower rates

- Reduced fees

- Better repayment terms

Online Business Loans vs Traditional Bank Loans

In 2026, many businesses now use online lenders instead of traditional banks.

Both options have advantages.

Online Business Loans

Advantages

- Faster approval

- Less paperwork

- Easier application process

- Funding within 24–72 hours

Disadvantages

- Higher interest rates

- Smaller loan amounts

- More expensive fees

Online lenders are popular among startups and small businesses needing quick cash flow support.

Traditional Bank Loans

Advantages

- Lower interest rates

- Better long-term financing

- More stable lending environment

Disadvantages

- Slower approval

- Stricter requirements

- More documentation

Banks are usually better for larger and long-term financing needs.

Common Business Loan Mistakes to Avoid

Many businesses create financial problems because they borrow incorrectly.

1. Borrowing Without a Clear Plan

Never take a loan without understanding exactly how the money will be used.

Poor planning increases financial risk.

2. Ignoring Total Loan Cost

Many borrowers focus only on monthly payments.

Always calculate:

- Interest cost

- Processing fees

- Hidden charges

- Penalties

The cheapest-looking loan is not always the best.

3. Overborrowing

Too much debt can damage cash flow and create repayment pressure.

Borrow only what your business can realistically manage.

4. Not Reading Terms Carefully

Always review:

- Repayment schedule

- Penalty clauses

- Interest structure

- Early repayment conditions

Understanding the agreement protects your business.

5. Mixing Personal and Business Expenses

Using business loans for personal spending creates financial instability and accounting problems.

Keep business finances separate.

Best Uses of Business Loans

Business financing should support growth and productivity.

Good Uses of Business Loans

- Expanding operations

- Purchasing equipment

- Hiring staff

- Inventory management

- Marketing campaigns

- Technology upgrades

- Opening new locations

These investments can help increase revenue and efficiency.

Poor Uses of Business Loans

Avoid using commercial financing for:

- Personal expenses

- Speculative investments

- Luxury spending

- Unplanned purchases

Bad borrowing decisions can hurt long-term business health.

Benefits of Business Loans

A well-managed business loan can provide several advantages.

1. Access to Capital

Business loans provide funding that may otherwise take years to save.

2. Supports Growth

Financing allows businesses to scale faster.

3. Improves Cash Flow

Working capital loans help businesses manage temporary financial pressure.

4. Builds Business Credit

Responsible repayment improves your commercial credit profile.

Strong business credit may help secure larger financing later.

Risks of Business Loans

Business financing also involves risks.

1. Debt Burden

Monthly repayments can pressure business cash flow.

2. High Interest Costs

Especially with unsecured or high-risk loans.

3. Collateral Risk

Defaulting on secured loans may result in asset loss.

4. Financial Stress

Poorly structured loans can damage long-term business stability.

Tips for First-Time Business Borrowers

If you are applying for your first business loan, follow these practical tips.

Start Small

Smaller loans are easier to manage and repay.

Maintain Proper Financial Records

Good bookkeeping improves credibility with lenders.

Build a Repayment History

Consistent repayment strengthens future financing opportunities.

Work With Trusted Lenders

Choose reputable lenders with transparent terms.

Avoid suspicious financing offers.

Improve Cash Flow Before Applying

Lenders prefer financially stable businesses.

Frequently Asked Questions (FAQs)

Q1: Can I get a business loan without collateral?

Yes, but unsecured loans usually have higher interest rates and stricter approval requirements.

Q2: What credit score is needed for a business loan?

Many lenders prefer scores above 650, but requirements vary depending on the lender and loan type.

Q3: Can startups qualify for business loans?

Yes, although approval is generally harder without strong revenue or business history.

Q4: Is it safe to apply for business loans online?

Yes, if you use reputable lenders and secure platforms.

Q5: How long does business loan approval take?

- Online lenders: usually 1–3 days

- Traditional banks: often 1–3 weeks

Q6: Should I choose secured or unsecured financing?

Secured loans usually offer lower rates, while unsecured loans provide faster access without collateral.

Final Thoughts: Smart Business Financing Builds Stronger Companies

A business loan should not simply solve a short-term cash problem. The right financing strategy can help your company grow, improve operations, increase revenue, and build long-term success.

The key is borrowing responsibly.

Before taking a business loan:

- Understand your financing needs

- Compare multiple lenders

- Review all fees and terms

- Borrow only what you can repay comfortably

- Create a realistic repayment plan

In 2026, business owners have more financing options than ever before — from banks and Islamic lenders to fintech platforms and online commercial financing companies.

But the smartest entrepreneurs are not the ones who borrow the most money. They are the ones who use financing strategically to create sustainable business growth without unnecessary financial stress.