Life is uncertain. No one can predict the future, which is exactly why financial planning matters so much. While people work hard to build a better life for their families, many forget one important question:

“What would happen to my loved ones financially if I were no longer there?”

This is where life insurance becomes essential.

Life insurance is not just another financial product. It is a long-term protection strategy designed to provide financial security to your family during difficult times. It can help your loved ones manage daily expenses, pay off debts, continue education plans, and maintain financial stability even after the loss of the family’s primary income earner.

Yet many people delay buying life insurance because they believe it is expensive, confusing, or unnecessary. Others purchase the wrong policy without fully understanding how it works.

This complete 2026 guide explains life insurance plans, benefits, premium costs, policy types, and smart buying tips in clear and practical language — so you can choose the right coverage for yourself and your family.

Whether you are a young professional, parent, business owner, or someone planning for long-term financial security, this guide will help you make a more informed decision.

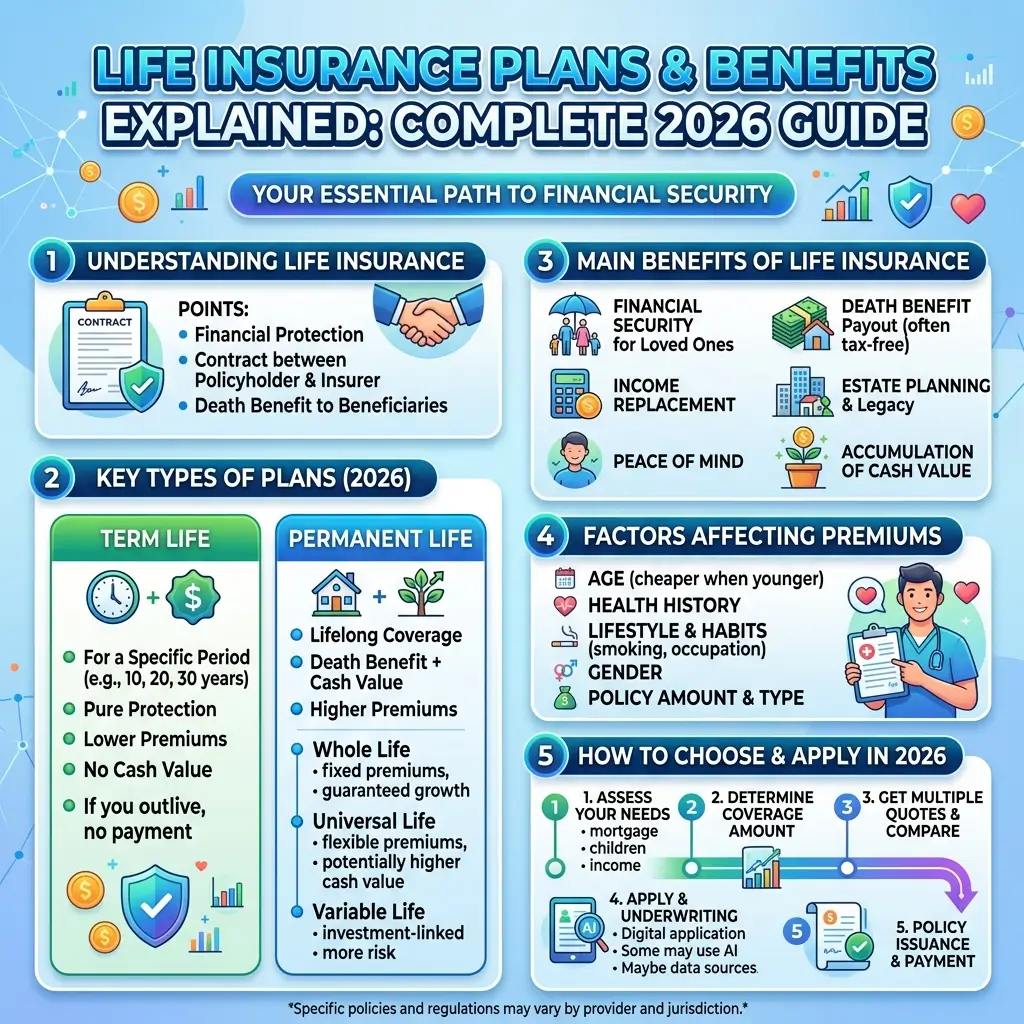

What Is Life Insurance?

Life insurance is a financial agreement between an individual and an insurance company.

In this agreement:

- You pay regular premiums to the insurer

- The insurance company provides financial coverage

- If the insured person passes away during the policy period, the insurer pays a lump sum amount to the family or nominee

This payout is commonly known as the death benefit or sum assured.

The main purpose of life insurance is to provide financial protection to your dependents if something unexpected happens to you.

How Life Insurance Works

Understanding how life insurance works is important before buying any policy.

Here’s a simple explanation.

Step 1: Choose a Policy

You select a life insurance plan based on:

- Coverage needs

- Budget

- Financial goals

- Policy duration

Step 2: Pay Premiums

You pay monthly, quarterly, or yearly premiums to the insurance company.

Premium amount depends on factors such as:

- Age

- Health

- Lifestyle

- Coverage amount

- Policy type

Step 3: Policy Remains Active

As long as premiums are paid on time, the policy stays active.

Step 4: Claim Process

If the insured person passes away during the policy term, the nominee submits a claim.

After verification, the insurer releases the payout to the beneficiaries.

Key Features of Life Insurance

Most life insurance plans include several important features.

Financial Protection for Dependents

The main purpose is to support your family financially after your death.

Flexible Premium Options

Many insurers offer flexible payment schedules.

Policy Duration Choices

Coverage may last:

- 10 years

- 20 years

- 30 years

- Entire lifetime

Death Benefit Payout

The insurer provides a tax-free or partially tax-free lump sum in many countries.

Why Life Insurance Is Important

Many people underestimate the financial impact a sudden loss can have on a family.

Life insurance helps reduce that financial burden.

1. Financial Security for Your Family

Your family may still need money for:

- Household expenses

- Rent or mortgage payments

- School fees

- Utility bills

- Daily living costs

Life insurance ensures they are financially supported.

2. Income Replacement

If you are the primary earning member of the family, your income supports your household.

Life insurance can replace lost income and help your family maintain their lifestyle.

3. Debt Protection

Outstanding debts do not disappear after death.

Life insurance can help pay off:

- Home loans

- Car loans

- Personal loans

- Business liabilities

This prevents financial pressure on surviving family members.

4. Peace of Mind

Knowing your loved ones are protected provides emotional and financial peace of mind.

This is one of the biggest reasons people choose life insurance.

Types of Life Insurance Plans

There are several different types of life insurance policies available in 2026.

Understanding the differences helps you choose the right plan for your needs.

1. Term Life Insurance

Term life insurance is the simplest and most affordable type of life insurance.

It provides protection for a specific period such as:

- 10 years

- 20 years

- 30 years

If the insured person dies during the policy term, the family receives the payout.

If the policy expires and the insured survives, there is usually no maturity benefit.

Advantages

- Low premium cost

- High coverage amount

- Simple structure

Disadvantages

- No investment or savings component

- No maturity payout

Best For

People who want maximum protection at the lowest cost.

2. Whole Life Insurance

Whole life insurance provides coverage for the insured’s entire lifetime.

It also includes a savings or cash-value component.

Advantages

- Lifetime coverage

- Wealth accumulation

- Cash value growth

Disadvantages

- Higher premiums

- More complex structure

Best For

People seeking lifelong protection and long-term financial planning.

3. Endowment Plans

Endowment plans combine insurance with savings.

If the insured survives the policy term, the insurer pays a maturity benefit.

If death occurs during the policy period, beneficiaries receive the insured amount.

Advantages

- Savings element

- Guaranteed maturity payout

Disadvantages

- Lower coverage compared to term plans

- Higher premiums

Best For

Individuals seeking both insurance and disciplined savings.

4. Unit Linked Insurance Plans (ULIPs)

ULIPs combine life insurance with investment opportunities.

Part of the premium goes toward insurance coverage, while another portion is invested in market-linked funds.

Advantages

- Investment growth potential

- Insurance coverage

- Flexibility

Risks

- Market fluctuations affect returns

- Management charges may apply

Best For

People comfortable with investment risk.

5. Islamic Life Insurance (Takaful)

In countries like Pakistan and many Muslim-majority regions, Islamic insurance solutions are increasingly popular.

Takaful is a Shariah-compliant alternative to conventional insurance.

Key Features

- Risk-sharing model

- Ethical investments

- No interest (riba)

- Mutual cooperation structure

Many individuals choose Takaful because it aligns with Islamic financial principles.

How Much Life Insurance Coverage Do You Need?

One of the most important questions is how much coverage is enough.

A common recommendation is:

👉 Life insurance coverage should equal 10 to 15 times your annual income.

However, this depends on your financial situation.

Consider:

- Number of dependents

- Children’s education costs

- Outstanding debts

- Household expenses

- Future financial goals

- Inflation

The goal is to provide enough financial support for your family to remain stable even in your absence.

Life Insurance Premiums in 2026

A premium is the amount you pay to maintain your policy.

Premiums vary significantly depending on multiple factors.

Factors That Affect Life Insurance Cost

1. Age

Age is one of the biggest pricing factors.

Younger individuals usually receive much lower premiums because they are considered lower risk.

Important Tip

Buying life insurance early can save substantial money over time.

2. Health Condition

Insurance companies evaluate medical history and current health.

Health issues may increase premiums or affect approval.

3. Lifestyle Habits

Certain habits increase insurance risk.

Examples include:

- Smoking

- Heavy alcohol use

- Dangerous occupations

- Extreme sports

Riskier lifestyles usually mean higher premiums.

4. Coverage Amount

Higher coverage naturally results in higher premiums.

5. Policy Type

Term insurance is generally cheaper than whole life or investment-linked policies.

How to Choose the Best Life Insurance Plan

Choosing the right policy requires careful planning.

Step 1: Define Your Goal

Ask yourself what you want from insurance.

If your goal is:

- Pure financial protection → Term insurance

- Long-term savings → Endowment plans

- Investment growth → ULIPs

- Shariah-compliant protection → Takaful

Step 2: Compare Multiple Policies

Never buy the first plan you see.

Compare:

- Premium costs

- Coverage amount

- Claim settlement ratio

- Policy benefits

- Exclusions

- Riders and add-ons

Comparison helps you find better value.

Step 3: Check the Insurance Company’s Reputation

Choose insurers with:

- Strong financial stability

- Good customer service

- High claim settlement ratio

- Positive market reputation

A reliable insurer matters just as much as the policy itself.

Benefits of Life Insurance

Life insurance provides several important financial benefits.

1. Financial Protection

The primary purpose is protecting your family financially.

2. Tax Benefits

In some countries, premiums and payouts may qualify for tax benefits.

Always check local tax regulations.

3. Wealth Creation

Certain policies build cash value or investment returns over time.

4. Loan Facility

Some life insurance plans allow policyholders to borrow against accumulated value.

5. Estate Planning

Life insurance can help transfer wealth to future generations efficiently.

Term Life Insurance vs Whole Life Insurance

Many buyers struggle to choose between term and whole life coverage.

Here’s a simple comparison.

| Feature | Term Insurance | Whole Life Insurance |

|---|---|---|

| Premium Cost | Lower | Higher |

| Coverage Duration | Fixed term | Lifetime |

| Savings Component | No | Yes |

| Maturity Benefit | No | Yes |

| Best For | Affordable protection | Long-term wealth planning |

For most families seeking affordable protection, term insurance is usually the best starting option.

Common Life Insurance Mistakes to Avoid

Many people make expensive mistakes because they buy insurance without proper understanding.

1. Buying Too Late

Premiums increase significantly with age.

Buying early locks in lower rates.

2. Choosing Insufficient Coverage

Low coverage may not adequately support your family.

3. Hiding Medical Information

Providing false health information can result in claim rejection later.

Always be honest during the application process.

4. Ignoring Policy Terms

Many buyers never read policy details carefully.

Always understand:

- Exclusions

- Waiting periods

- Premium obligations

- Claim conditions

5. Not Comparing Insurers

Different companies may offer significantly different pricing and benefits.

When Should You Buy Life Insurance?

The best time to buy life insurance is usually as early as possible.

Life insurance becomes especially important when:

- You start earning

- You get married

- You have children

- You take a home loan

- Family members depend on your income

Buying early usually means:

- Lower premiums

- Easier approval

- Better long-term value

Life Insurance Claim Process Explained

Understanding the claim process helps families avoid confusion during difficult times.

Step 1: Inform the Insurance Company

The nominee contacts the insurer and reports the death.

Step 2: Submit Required Documents

Typical documents include:

- Death certificate

- Policy documents

- Identity verification

- Medical records if required

Step 3: Verification Process

The insurer reviews and verifies the claim.

Step 4: Payout Release

Once approved, the payout is transferred to the nominee or beneficiaries.

Documents Required for Life Insurance

Common documentation includes:

- National ID or passport

- Income proof

- Medical reports

- Address verification

- Nominee details

- Employment information

Requirements vary depending on the insurer and policy type.

Is Life Insurance Worth It?

For most people with financial responsibilities, yes.

Without life insurance:

- Families may struggle financially

- Debts can become overwhelming

- Long-term goals may collapse

With proper life insurance:

- Dependents remain financially protected

- Loans and expenses can still be managed

- Family stability improves

Life insurance is ultimately about protecting the people who depend on you.

Frequently Asked Questions (FAQs)

Q1: What is the best life insurance plan in 2026?

For affordable financial protection, term life insurance is often considered the best option for most families.

Q2: How much life insurance coverage should I buy?

A common recommendation is 10–15 times your annual income, adjusted for debts and family needs.

Q3: Is Takaful better than conventional insurance?

It depends on your personal and religious preferences. Takaful offers Shariah-compliant protection structures.

Q4: Can I cancel my life insurance policy?

Yes, but cancellation terms vary depending on the policy type and duration.

Q5: Does life insurance cover natural death?

Most standard policies cover natural death, subject to policy terms and waiting periods.

Q6: Why are premiums cheaper at a younger age?

Younger individuals are statistically considered lower risk by insurers.

Final Thoughts: Life Insurance Is Financial Responsibility, Not Just Protection

Life insurance is not just about money. It is about responsibility, planning, and protecting the people who matter most.

Many people spend years building careers, buying homes, and creating better opportunities for their families — but fail to protect those goals financially.

The right life insurance plan ensures that your loved ones can continue moving forward even during the most difficult circumstances.

In 2026, buyers have more options than ever, including:

- Affordable term insurance

- Lifetime coverage plans

- Investment-linked policies

- Shariah-compliant Takaful solutions

The key is choosing a plan that fits your financial goals, budget, and family responsibilities.

Start early, compare carefully, understand your policy fully, and choose protection that provides real long-term security for the people who depend on you.