Buying a car is one of the biggest financial decisions most people make. Whether you are purchasing your first vehicle, upgrading to a family car, or investing in a reliable daily commute, the cost of buying a vehicle outright is often too high for many buyers.

That is why millions of people rely on car loans and auto financing to make vehicle ownership possible.

But here’s the problem: many buyers focus only on monthly payments and ignore the bigger financial picture. As a result, they end up paying extremely high interest rates, hidden charges, and unnecessary financing costs that add up over several years.

The good news is that getting a low interest car loan in 2026 is possible if you understand how auto financing works and make smart financial decisions before signing any agreement.

This complete car loan guide explains everything you need to know about low-interest auto financing, including how car loans work, how lenders calculate rates, how to qualify for better financing, Islamic car financing options, common mistakes to avoid, and practical ways to save money over the life of your loan.

If you are planning to finance a vehicle in 2026, this guide will help you make a smarter and more financially responsible decision.

What Is a Car Loan?

A car loan, also called an auto loan, is a type of financing that helps individuals purchase a vehicle without paying the full price upfront.

Instead of paying the entire amount immediately, a lender such as a bank, Islamic financial institution, or online lender pays for the vehicle on your behalf. You then repay the lender through monthly installments over a fixed period.

These monthly payments are commonly known as EMIs (Equated Monthly Installments).

A car loan typically includes:

- Principal amount (loan amount)

- Interest charges

- Loan tenure

- Monthly installment schedule

In most cases, the car itself acts as collateral for the loan. This means the lender can repossess the vehicle if payments are not made on time.

How Car Loans Work

Understanding how auto financing works can help you avoid expensive mistakes.

Here’s a simplified breakdown.

Step 1: Choose the Vehicle

First, you select the car you want to buy.

The lender may consider:

- Vehicle price

- Brand

- Model year

- New or used condition

- Resale value

Step 2: Apply for Financing

You submit a loan application to a bank, lender, or financing company.

The lender evaluates:

- Income

- Employment stability

- Credit history

- Existing debt

- Down payment amount

Step 3: Loan Approval

If approved, the lender offers:

- Loan amount

- Interest rate

- Loan tenure

- Monthly payment amount

Step 4: Vehicle Purchase

The lender pays the dealership or seller.

You receive the vehicle and begin making monthly payments.

Step 5: Repayment

You repay the loan in installments over the agreed period.

Once the loan is fully paid, ownership transfers completely to you if applicable.

Key Features of Car Loans

Most auto loans include several standard features.

Fixed Loan Amount

The lender approves a specific amount based on your financial profile.

Monthly Installments (EMIs)

You repay the loan through fixed monthly payments.

Loan Tenure

Most car loans range between:

- 1 year

- 3 years

- 5 years

- 7 years

Longer tenure reduces monthly payments but increases total interest cost.

Interest Charges

Interest is the cost of borrowing money.

The interest rate significantly affects the total amount you repay.

Types of Car Loans in 2026

Different financing options are available depending on the type of vehicle and borrower profile.

1. New Car Loans

New car financing is designed for brand-new vehicles.

Advantages

- Lower interest rates

- Easier approval process

- Longer repayment terms

- Better financing offers

Lenders usually prefer financing new cars because they have higher resale value and lower risk.

2. Used Car Loans

Used car loans are designed for pre-owned vehicles.

Advantages

- Lower vehicle cost

- Smaller loan amount

Disadvantages

- Higher interest rates

- Shorter loan tenure

- Stricter vehicle age limits

Used car financing is generally more expensive because older cars carry higher risk for lenders.

3. Secured Car Loans

In secured financing, the car acts as collateral.

Benefits

- Lower interest rates

- Higher approval chances

- Larger financing amounts

This is the most common form of auto financing.

4. Pre-Approved Car Loans

Some banks offer pre-approved loans to existing customers.

Benefits

- Faster approval

- Easier documentation

- Better negotiation power at dealerships

Pre-approval also helps buyers understand their budget before shopping for a vehicle.

Why a Low Interest Rate Matters

Many buyers underestimate how much interest affects total car cost.

Even a small difference in interest rate can save thousands over time.

For example:

- A 10% interest loan

- Versus a 15% interest loan

can create a massive difference over a 5-year repayment period.

Lower interest rates mean:

- Smaller monthly payments

- Lower total repayment cost

- Faster debt reduction

- Better financial flexibility

This is why comparing loan offers carefully is extremely important.

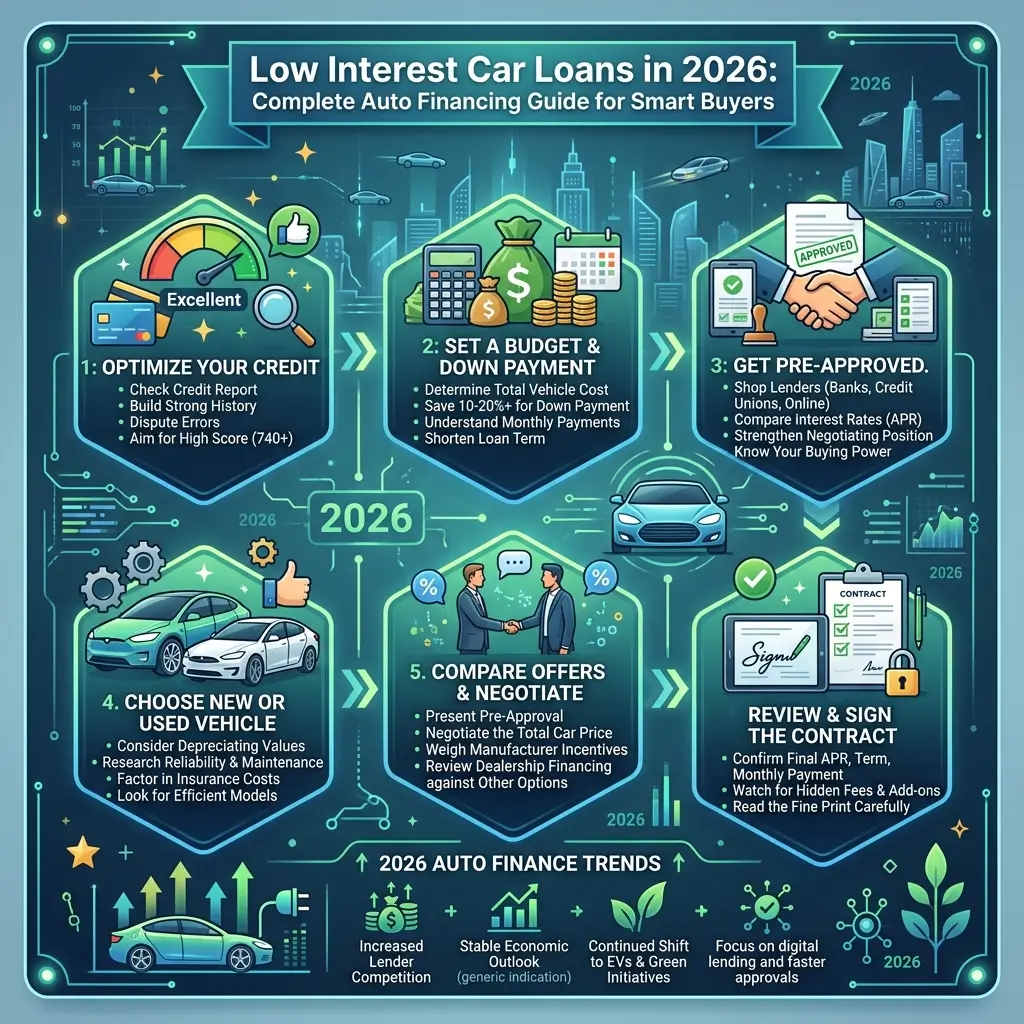

How to Get a Low Interest Car Loan

Securing a low-interest car loan is not just about luck. It depends on preparation, financial habits, and negotiation.

Here are the most effective strategies.

Step 1: Check Your Credit Score

Your credit score is one of the most important factors lenders consider.

A higher credit score usually means:

- Lower interest rates

- Faster approvals

- Better loan terms

Lenders see high-credit borrowers as less risky.

Step 2: Compare Multiple Lenders

Never accept the first financing offer without comparison.

Compare rates from:

- Traditional banks

- Islamic banks

- Online lenders

- Credit unions

- Dealer financing companies

Even a small rate difference matters over several years.

Step 3: Make a Larger Down Payment

A down payment is the upfront amount you pay before financing begins.

A larger down payment:

- Reduces loan amount

- Lowers lender risk

- Improves interest rates

- Reduces monthly installments

Experts often recommend putting down at least 20%.

Step 4: Choose a Shorter Loan Tenure

Shorter loans usually have lower interest rates.

Benefits

- Less total interest paid

- Faster ownership

- Lower overall cost

Drawback

- Higher monthly payments

Choose a balance between affordability and total financing cost.

Step 5: Get Pre-Approved

Loan pre-approval gives you stronger negotiating power when buying a vehicle.

It also helps you:

- Avoid dealer pressure

- Understand your budget

- Compare financing options more effectively

Car Loan Interest Rates in 2026

Interest rates vary depending on several financial factors.

Typical car loan rates in 2026 may include:

| Credit Profile | Typical Interest Rate |

|---|---|

| Excellent Credit | 7% – 10% |

| Good Credit | 10% – 15% |

| Average Credit | 15% – 22% |

| Poor Credit | 22%+ |

These rates can vary based on:

- Country

- Central bank policies

- Economic conditions

- Vehicle type

- Loan duration

- Lender policies

Factors That Affect Your Auto Loan Rate

Several elements influence your financing offer.

1. Credit Score

This is often the most important factor.

Better credit usually equals lower interest.

2. Income Stability

Stable income reassures lenders that you can repay the loan consistently.

3. Loan Amount

Larger loans increase lender risk.

This can lead to higher rates.

4. Vehicle Type

New vehicles usually receive better rates than older used vehicles.

Luxury cars may also carry different financing conditions.

5. Down Payment

Higher down payments reduce lender exposure and often improve financing terms.

Understanding EMI (Monthly Payments)

Your EMI depends on three main factors:

- Loan amount

- Interest rate

- Loan tenure

Important Rule

Longer tenure may lower monthly payments, but it increases total interest paid over time.

Many buyers focus only on affordable EMIs without calculating the overall financing cost.

That can become an expensive mistake.

Documents Required for Car Loans

Most lenders require standard financial and identity documents.

Common requirements include:

- National ID card or passport

- Income proof

- Salary slips

- Bank statements

- Employment details

- Tax documents

- Vehicle quotation or details

Self-employed applicants may need additional financial records.

Benefits of Car Loans

Auto financing offers several advantages when managed responsibly.

1. Immediate Car Ownership

Car loans allow buyers to purchase vehicles without waiting years to save the full amount.

2. Flexible Repayment

Most lenders offer different tenure options to match varying budgets.

3. Builds Credit History

Making timely payments can improve your credit profile.

Good credit helps with future financing opportunities.

4. Preserves Cash Flow

Instead of spending all savings on a car, financing allows buyers to keep liquidity for emergencies or investments.

Risks of Car Loans

Car financing also carries important financial risks.

1. High Interest Costs

Long loan terms can significantly increase the total cost of the vehicle.

2. Vehicle Depreciation

Cars lose value over time.

In some cases, borrowers owe more than the car is worth.

3. Repossession Risk

Failure to make payments can result in vehicle seizure by the lender.

4. Financial Pressure

Large monthly payments may strain your budget if income changes unexpectedly.

How Much Car Loan Can You Afford?

One of the biggest mistakes buyers make is financing more than they can realistically afford.

A commonly recommended rule is:

👉 Your car EMI should not exceed 15% to 20% of your monthly income.

This helps maintain financial stability and reduces debt stress.

You should also account for:

- Fuel

- Insurance

- Maintenance

- Registration fees

- Parking

- Unexpected repairs

Car ownership costs more than just the monthly loan payment.

Islamic Car Financing Options

In countries like Pakistan and many Muslim-majority regions, Islamic auto financing has become increasingly popular.

These financing methods avoid traditional interest-based lending.

1. Ijarah (Islamic Leasing)

Under Ijarah:

- The bank purchases the vehicle

- The customer leases it

- Ownership transfers after the agreement ends

Benefits

- Shariah-compliant

- Transparent structure

- Fixed payment schedule

2. Diminishing Musharakah

This structure involves shared ownership between the bank and customer.

Over time, the customer gradually purchases the bank’s ownership share.

Benefits

- Ethical financing structure

- Shared ownership model

- Increasingly common in Islamic banking

Islamic financing appeals to buyers seeking religiously compliant financial solutions.

Online Financing vs Dealer Financing

Buyers often choose between direct lender financing and dealership financing.

Online or Bank Financing

Advantages

- Lower interest rates

- Transparent terms

- Better comparison opportunities

Disadvantages

- More paperwork

- Longer approval process

Dealer Financing

Advantages

- Convenient

- Faster processing

- Promotional offers

Disadvantages

- Higher interest rates

- Hidden costs possible

- Less negotiation transparency

Always compare dealer offers with independent lenders before making a decision.

Common Car Loan Mistakes to Avoid

Many buyers pay far more than necessary because of avoidable mistakes.

1. Not Comparing Loan Offers

Different lenders may offer very different rates.

Always compare financing options carefully.

2. Focusing Only on EMI

Low monthly payments can hide expensive long-term interest costs.

Always calculate the total repayment amount.

3. Choosing Extremely Long Loan Terms

Long tenure reduces EMI but increases total interest dramatically.

4. Ignoring Hidden Fees

Check for:

- Processing fees

- Insurance charges

- Documentation fees

- Late payment penalties

- Prepayment charges

Hidden costs can increase overall financing expenses.

Tips to Save Money on Car Loans

Smart financial habits can significantly reduce auto loan costs.

Increase Your Down Payment

Larger upfront payments reduce borrowing needs.

Improve Your Credit Score

Better credit often results in lower interest rates.

Choose Shorter Loan Tenure

Shorter loans reduce overall interest payments.

Avoid Unnecessary Add-Ons

Dealers may push expensive extras like:

- Extended warranties

- Accessories

- Insurance bundles

Only pay for what you truly need.

Refinance if Better Rates Become Available

Some borrowers refinance existing loans at lower rates later.

This may reduce monthly payments or total interest.

Frequently Asked Questions (FAQs)

Q1: What is considered a good car loan interest rate in 2026?

A good rate depends on your credit profile, market conditions, and lender. Borrowers with excellent credit usually receive the best offers.

Q2: Can I get a car loan with poor credit?

Yes, but interest rates are usually much higher.

Improving your credit before applying can help significantly.

Q3: Is Islamic car financing better than conventional financing?

It depends on your financial and religious preferences. Many buyers prefer Islamic financing for Shariah compliance and transparent structures.

Q4: Can I repay my car loan early?

Yes, many lenders allow early repayment. However, some may charge prepayment penalties.

Always check the loan terms carefully.

Q5: Should I finance through a dealer or a bank?

Banks often offer lower rates, while dealers provide convenience. Comparing both options is usually the smartest approach.

Final Thoughts: Smart Financing Can Save You Thousands

Buying a car is exciting, but financing decisions can affect your finances for years.

A low-interest car loan is not just about getting approved. It is about understanding the full cost of borrowing and choosing a financing structure that supports your long-term financial health.

The smartest borrowers:

- Compare lenders carefully

- Improve their credit before applying

- Avoid unnecessarily long loan terms

- Make larger down payments

- Understand every fee and condition

In 2026, car financing options are more accessible than ever, including conventional loans, online financing, and Islamic auto financing solutions.

If you take time to research your options and make informed decisions, you can enjoy vehicle ownership while avoiding unnecessary financial stress and saving a significant amount of money over the life of your loan.