Personal loans have become one of the most popular financial products in the world. In 2026, millions of people use personal loans to handle emergencies, consolidate debt, pay medical expenses, renovate homes, fund education, or manage short-term financial needs.

The reason is simple: personal loans provide fast access to money without requiring complicated collateral in most cases.

But there is also a major risk.

Many borrowers end up paying extremely high interest rates, hidden charges, and unnecessary fees because they apply without understanding how personal loans actually work. Some people choose the first offer they receive, while others focus only on monthly payments and ignore the total cost of borrowing.

The result can be years of unnecessary financial stress.

This complete personal loan guide explains how low-interest personal loans work, how lenders calculate rates, what affects approval, and how to avoid expensive borrowing mistakes.

Whether you need emergency funds, debt consolidation, or flexible financing for a major expense, this guide will help you make smarter financial decisions and find better loan offers in 2026.

What Is a Personal Loan?

A personal loan is a type of financing that allows individuals to borrow money for almost any purpose.

Unlike home loans or car loans, personal loans are usually unsecured. This means borrowers generally do not need to provide collateral such as property or vehicles.

Once approved, the lender provides a lump-sum amount, and the borrower repays the loan through fixed monthly installments over a specific period.

Personal loans are commonly used for:

- Medical emergencies

- Debt consolidation

- Home improvement

- Weddings

- Education expenses

- Travel

- Unexpected bills

- Business support

- Major purchases

Because personal loans are flexible, they are widely used around the world.

Key Features of Personal Loans

Most personal loans include several standard features.

No Collateral Required

Most personal loans are unsecured, meaning you do not need to risk assets like your house or car.

Fixed Monthly Payments

Borrowers usually repay loans through predictable monthly EMIs.

Flexible Loan Usage

Unlike specialized loans, personal loans can be used for multiple purposes.

Fixed or Variable Interest Rates

Some lenders offer fixed interest rates, while others provide variable-rate loans.

Short-to-Medium Loan Tenure

Most personal loans are repaid within 1 to 5 years.

Why Personal Loans Are So Popular

Personal loans continue to grow in popularity because they are accessible, flexible, and relatively fast.

1. Quick Access to Cash

Many lenders approve personal loans quickly.

In 2026:

- Online lenders may approve within 24–48 hours

- Banks may take 2–5 days

This makes personal loans useful during emergencies.

2. Flexible Usage

Unlike home or car financing, personal loans can usually be used for almost any legal purpose.

This flexibility attracts many borrowers.

3. No Collateral Requirement

Borrowers can access financing without risking major assets.

This is especially useful for people who do not own property.

4. Fixed Repayment Schedule

Fixed monthly payments help borrowers plan their budget more easily.

Types of Personal Loans

Understanding different personal loan types helps you choose the right financing option.

1. Unsecured Personal Loans

Unsecured loans do not require collateral.

Advantages

- Faster approval

- No asset risk

- Simple application process

Disadvantages

- Higher interest rates

- Lower borrowing limits

Best For

Borrowers with stable income and good credit scores.

2. Secured Personal Loans

Secured loans require collateral such as:

- Savings accounts

- Vehicles

- Property

- Investments

Advantages

- Lower interest rates

- Easier approval

- Larger loan amounts

Disadvantages

- Risk of losing collateral

Best For

Borrowers seeking lower rates or larger financing.

3. Debt Consolidation Loans

Debt consolidation loans combine multiple debts into one single loan.

This helps simplify repayment and may reduce overall interest costs.

Common Uses

- Credit card debt consolidation

- Paying off multiple personal loans

- Simplifying finances

Benefits

- Single monthly payment

- Easier debt management

- Potentially lower interest rate

4. Payday Loans (High-Risk Option)

Payday loans are short-term loans with extremely high interest rates.

Risks

- Very expensive borrowing

- Short repayment period

- Debt cycle risk

Recommendation

Most financial experts recommend avoiding payday loans whenever possible.

How Personal Loan Interest Rates Work

Interest is the cost of borrowing money.

The lender charges interest based on the borrower’s risk profile.

In 2026, average personal loan rates may include:

| Credit Profile | Typical Interest Rate |

|---|---|

| Excellent Credit | 8% – 12% |

| Good Credit | 12% – 18% |

| Average Credit | 18% – 30% |

| Poor Credit | 30%+ |

Rates vary depending on:

- Credit score

- Income

- Employment stability

- Existing debt

- Loan amount

- Loan tenure

- Country and market conditions

APR vs Interest Rate: What’s the Difference?

Many borrowers focus only on the interest rate.

But APR (Annual Percentage Rate) is more important.

APR includes:

- Interest charges

- Processing fees

- Additional loan costs

This gives a more accurate picture of the total loan cost.

Always compare APR instead of only looking at advertised interest rates.

Factors That Affect Your Personal Loan Interest Rate

Lenders evaluate several factors before deciding your rate.

1. Credit Score

Your credit score is one of the biggest factors.

Higher credit score:

- Lower interest rates

- Better approval chances

- Higher loan limits

Lower credit score:

- Higher interest rates

- Stricter conditions

Maintaining strong credit can save a large amount over time.

2. Income Level

Lenders prefer borrowers with stable and reliable income.

Higher income improves repayment confidence.

3. Employment Status

Salaried employees often receive better rates because lenders see them as more stable.

Self-employed individuals may face:

- Higher scrutiny

- More documentation

- Slightly higher rates

4. Existing Debt

Too much existing debt reduces loan eligibility.

Lenders check your debt-to-income ratio to determine affordability.

5. Loan Amount and Tenure

Longer loans often result in higher total interest costs.

Larger loans may also increase lender risk.

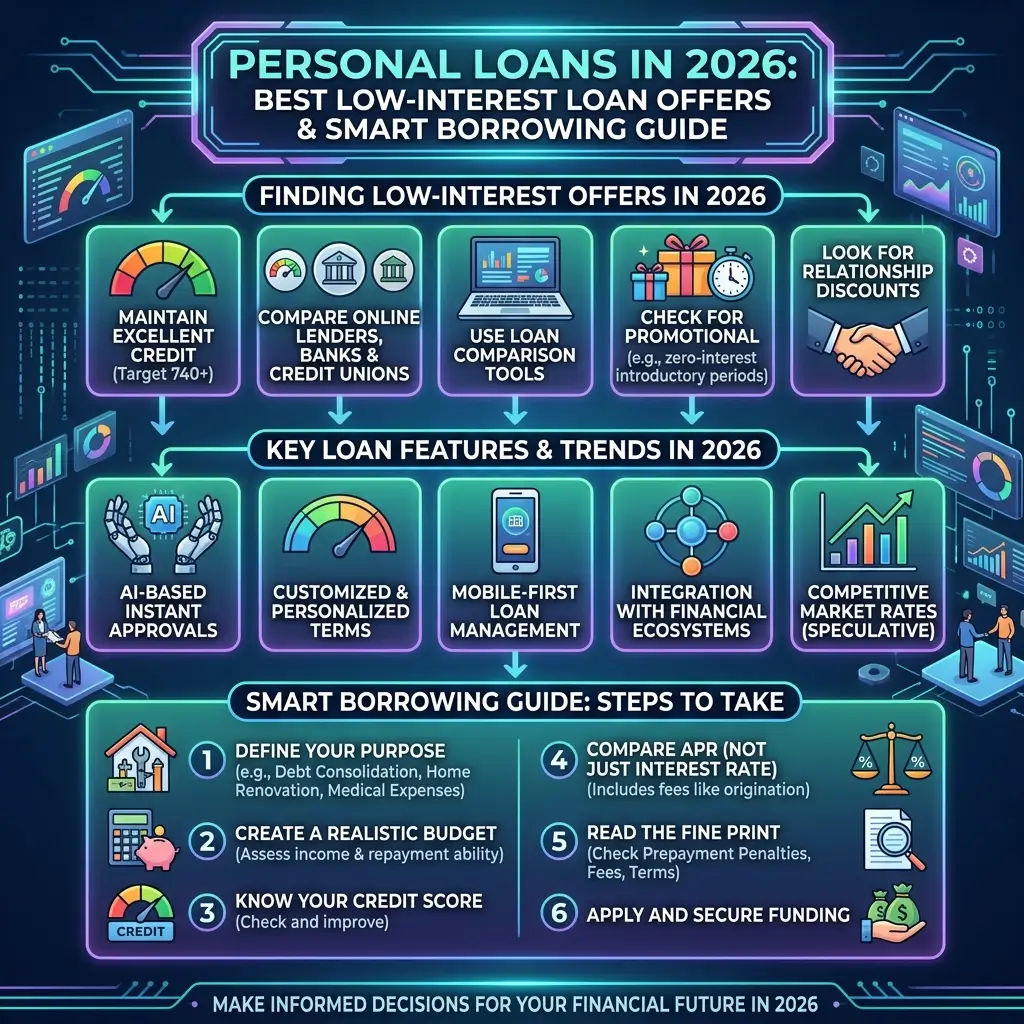

How to Find the Best Low-Interest Personal Loan

Finding a low-interest loan requires preparation and comparison.

Step 1: Compare Multiple Lenders

Never accept the first loan offer you receive.

Compare:

- Banks

- Online lenders

- Credit unions

- Financial institutions

- Fintech platforms

Even small rate differences can save substantial money.

Step 2: Compare APR, Not Just Interest

APR provides the real borrowing cost.

A loan with a lower interest rate but high fees may actually be more expensive.

Step 3: Choose the Right Loan Tenure

Shorter tenure:

- Higher EMI

- Lower total interest

Longer tenure:

- Lower EMI

- Higher total repayment cost

Choose a repayment period that balances affordability with long-term savings.

Step 4: Improve Your Credit Score Before Applying

Better credit usually means better loan offers.

To improve your score:

- Pay bills on time

- Reduce credit card balances

- Avoid missed payments

- Limit unnecessary loan applications

Step 5: Use Pre-Approved Offers

Banks sometimes provide lower rates to existing customers.

Pre-approved loans may also have:

- Faster processing

- Reduced documentation

- Better terms

How to Calculate Your Monthly Payment (EMI)

Your EMI depends on three main factors:

- Loan amount

- Interest rate

- Loan tenure

Important Tip

Lower monthly payments are not always better.

Longer repayment periods increase total interest paid.

Always calculate:

- Monthly affordability

- Total repayment cost

before accepting any loan.

Smart Ways to Get a Lower Personal Loan Interest Rate

Reducing your interest rate can save thousands over time.

1. Maintain a Strong Credit Score

This is one of the most effective ways to secure lower rates.

2. Apply With a Co-Applicant

A financially strong co-borrower may improve approval chances and reduce rates.

3. Choose a Shorter Loan Tenure

Shorter repayment periods usually reduce total borrowing cost.

4. Negotiate With Lenders

Many borrowers do not realize rates may be negotiable.

Strong applicants often qualify for better terms.

5. Reduce Existing Debt Before Applying

Lower debt improves your financial profile.

Benefits of Personal Loans

Personal loans offer several important advantages.

1. Fast Approval

Funds are often available quickly.

2. Flexible Usage

Borrowers can use funds for many purposes.

3. Predictable Payments

Fixed EMIs simplify budgeting.

4. No Collateral in Most Cases

Borrowers do not risk losing major assets.

5. Debt Consolidation Opportunity

Personal loans can help simplify high-interest debt.

Risks and Disadvantages of Personal Loans

Despite their convenience, personal loans also carry risks.

1. High Interest Rates

Especially for borrowers with weak credit profiles.

2. Fees and Penalties

Common charges include:

- Processing fees

- Late payment fees

- Prepayment penalties

3. Debt Trap Risk

Taking multiple loans simultaneously can become financially dangerous.

4. Credit Score Damage

Missed payments negatively affect your credit history.

Best Uses of Personal Loans

Personal loans should ideally be used for productive or necessary expenses.

Good Uses of Personal Loans

- Medical emergencies

- Debt consolidation

- Home repairs

- Education expenses

- Necessary family expenses

These uses may provide long-term value or financial stability.

Poor Uses of Personal Loans

Avoid using personal loans for:

- Luxury shopping

- Expensive vacations

- Gambling

- Impulse purchases

Borrowing for unnecessary spending can create long-term debt problems.

Common Personal Loan Mistakes to Avoid

Many borrowers make expensive errors because they rush into borrowing decisions.

1. Not Comparing Offers

Always compare multiple lenders before choosing.

2. Ignoring Hidden Charges

Check carefully for:

- Processing fees

- Insurance charges

- Prepayment penalties

- Late payment fees

3. Borrowing More Than Needed

Only borrow what you can comfortably repay.

4. Missing Payments

Late payments can increase costs and damage your credit score.

5. Focusing Only on Monthly EMI

A low EMI may hide a very long and expensive repayment structure.

Online Personal Loans vs Traditional Bank Loans

Borrowers now have more financing options than ever.

Online Lenders

Advantages

- Fast approval

- Easy application process

- Flexible eligibility

Disadvantages

- Slightly higher rates

- More fintech-related fees possible

Online lending is especially popular for quick financing.

Traditional Banks

Advantages

- Lower interest rates

- More reliable institutions

- Better long-term credibility

Disadvantages

- Slower approval

- Stricter documentation

Banks are often better for borrowers with strong financial profiles.

Documents Required for a Personal Loan

Most lenders require basic financial and identity documents.

Typical requirements include:

- National ID or passport

- Salary slips

- Bank statements

- Employment details

- Address verification

- Tax records in some cases

Self-employed applicants may need business records or additional financial proof.

How Long Does Personal Loan Approval Take?

Approval speed depends on the lender.

Typical timelines:

| Lender Type | Approval Time |

|---|---|

| Online lenders | 24–48 hours |

| Traditional banks | 2–5 days |

Some pre-approved offers may be even faster.

Who Should Consider a Personal Loan?

Personal loans may be suitable for:

- Salaried individuals

- Borrowers with stable income

- People managing temporary financial needs

- Individuals consolidating high-interest debt

They may not be ideal for people already struggling with heavy debt.

Tips for First-Time Borrowers

If you are applying for your first personal loan, follow these practical tips.

Borrow Conservatively

Only borrow what you truly need.

Read the Full Agreement

Understand:

- Interest structure

- Repayment schedule

- Penalties

- Fees

Maintain Emergency Savings

Do not rely entirely on loans for emergencies.

Avoid Multiple Simultaneous Loans

Too much debt creates financial pressure.

Build Strong Credit Habits

Responsible borrowing improves future financing opportunities.

Frequently Asked Questions (FAQs)

Q1: What credit score is needed for a personal loan?

Many lenders prefer scores above 650 for better rates, although requirements vary.

Q2: Can I get a personal loan with bad credit?

Yes, but interest rates will usually be significantly higher.

Q3: Is it safe to apply for loans online?

Yes, if you use trusted and reputable lenders.

Q4: Can I repay my personal loan early?

Yes, but some lenders charge prepayment penalties.

Always review the loan agreement carefully.

Q5: Are personal loans better than credit cards?

For large expenses or debt consolidation, personal loans may offer lower rates and structured repayment.

Q6: What happens if I miss a payment?

Late payments may result in:

- Penalties

- Higher interest

- Credit score damage

- Collection action

Final Thoughts: A Personal Loan Should Help You — Not Hurt You

Personal loans can be extremely useful financial tools when used responsibly.

They can help you manage emergencies, consolidate debt, improve your home, or handle important life expenses without selling assets or disrupting long-term savings.

But smart borrowing matters.

The best low-interest personal loan is not simply the fastest loan or the biggest loan. It is the one that fits your financial situation, repayment ability, and long-term stability.

Before taking any loan:

- Compare multiple lenders

- Understand the full cost

- Review all fees and conditions

- Borrow only what you truly need

- Choose a repayment plan you can comfortably manage

In 2026, borrowers have more financing options than ever before. The key is choosing carefully and borrowing strategically so your loan solves financial problems instead of creating bigger ones later.