Education has always been one of the most powerful investments a person can make. A good degree, professional certification, or specialized skill can open doors to better career opportunities, higher income, and long-term financial stability. But in 2026, the rising cost of education has made it increasingly difficult for many students and families to pay for studies without financial support.

That’s where student loans come in.

Whether you’re planning to study locally or abroad, understanding how education financing works is essential. A student loan can help you achieve your academic goals, but poor borrowing decisions can also create years of financial pressure after graduation.

This complete student loan guide explains everything you need to know about education financing in 2026 — including how student loans work, interest rates, eligibility, repayment strategies, and smart borrowing tips that can save you thousands over time.

If you are a student, parent, or future international applicant looking for practical and realistic advice, this guide will help you make informed financial decisions.

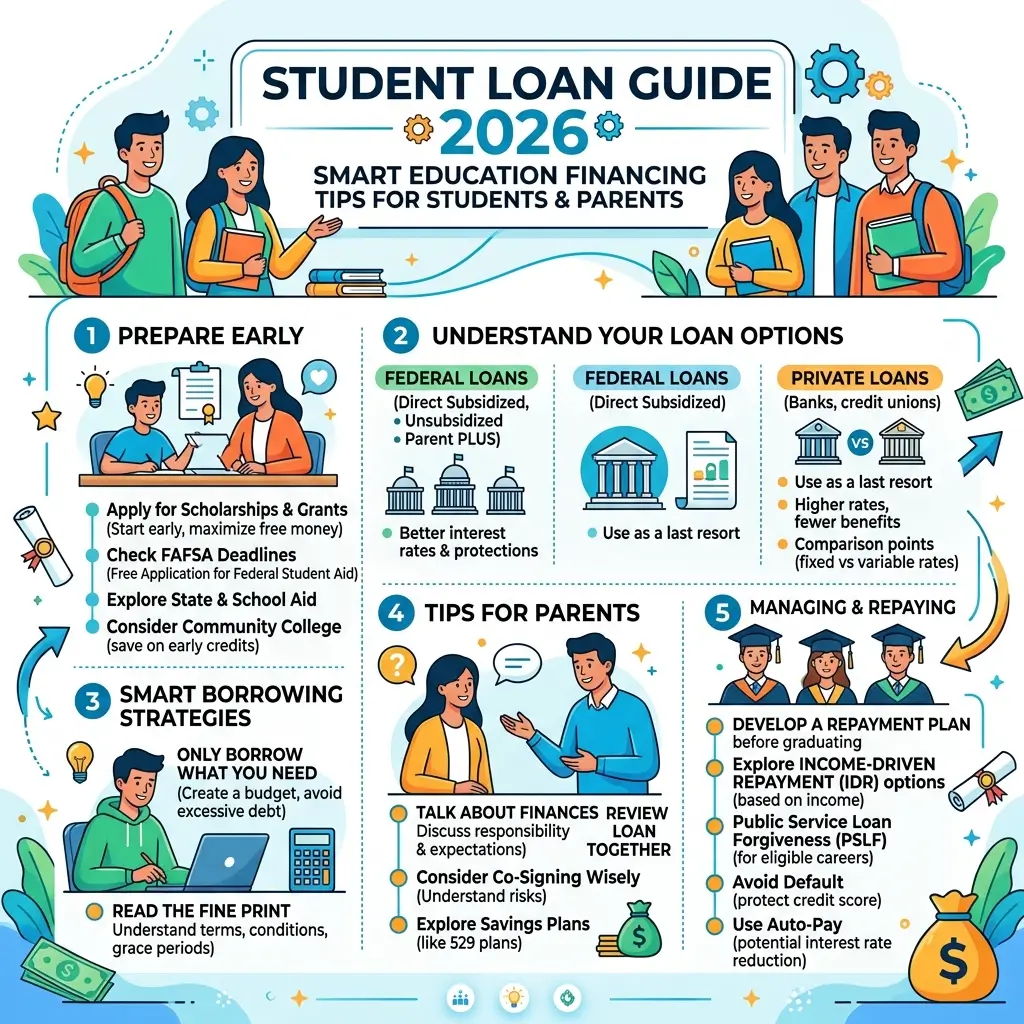

What Is a Student Loan?

A student loan is a type of financial assistance designed specifically to help students pay for education-related expenses.

Instead of paying all educational costs upfront, students borrow money from a government program, bank, or private lender and repay it later — usually after completing their studies.

Student loans are commonly used for:

- Tuition fees

- Hostel or accommodation expenses

- Books and study materials

- Transportation

- Laptop and academic equipment

- Daily living expenses

- Study abroad costs

Unlike scholarships or grants, student loans must be repaid, often with interest.

The main advantage is that students can access quality education immediately without waiting years to save enough money.

Why Student Loans Are More Important in 2026

Education costs have increased significantly across the world. Universities are charging higher tuition fees, inflation has raised living expenses, and studying abroad now requires a much larger financial commitment than before.

Because of this, education financing has become essential for many families.

In 2026, student loans are especially important for:

- International students

- Digital learning programs

- Medical and engineering students

- Students pursuing postgraduate degrees

- Families facing economic pressure

- Students attending private universities

At the same time, lenders have introduced more flexible financing options, including income-based repayment plans and Islamic education financing models.

This means students now have more choices — but they also need to understand the risks before borrowing.

Types of Student Loans in 2026

Not all student loans work the same way. Choosing the right loan type can significantly reduce your repayment burden in the future.

1. Government Student Loans

Government-backed student loans are usually considered the safest and most affordable option.

These loans are supported by the state and often come with lower interest rates and flexible repayment terms.

Key Benefits

- Lower interest rates

- Easier repayment schedules

- Grace period after graduation

- Subsidized interest in some cases

- Income-based repayment options

Best For

- Local university students

- Middle-income families

- Students needing long-term repayment flexibility

Government loans are generally the first option students should explore before considering private lenders.

2. Private Student Loans

Private education loans are offered by banks, fintech lenders, and financial institutions.

These loans can provide larger funding amounts, especially for international education, but they often come with higher interest rates and stricter conditions.

Features of Private Student Loans

- Faster approval process

- Larger borrowing limits

- Higher interest rates

- Credit score evaluation

- Co-signer or guarantor requirements

Best For

- Students studying abroad

- Students without access to government aid

- High-cost degree programs

Private loans can be useful, but students must carefully compare offers before signing any agreement.

3. Islamic Student Financing

In many Muslim-majority countries, students prefer Shariah-compliant financing solutions instead of traditional interest-based loans.

Islamic student financing uses ethical structures that avoid conventional interest (riba).

Common Features

- Interest-free structures

- Profit-sharing or service-based models

- Ethical financing principles

- Transparent repayment terms

Best For

- Students seeking halal financing options

- Families preferring Islamic banking systems

Islamic education financing has become increasingly popular in 2026, especially in Pakistan, the Middle East, and parts of Southeast Asia.

How Student Loans Work

Understanding the loan process is extremely important before applying.

Here’s a simple step-by-step breakdown of how student loans work.

Step 1: Apply for the Loan

The student submits an application along with required documents.

Lenders usually evaluate:

- Academic history

- Admission confirmation

- Financial background

- Family income

- Credit profile of co-signer

Step 2: Loan Review and Approval

The lender checks whether the applicant qualifies for financing.

Important factors include:

- University reputation

- Degree program

- Expected future income

- Financial need

- Creditworthiness

Approval times vary depending on the lender.

Step 3: Funds Disbursement

Once approved, the money is released.

The funds may be sent:

- Directly to the university

- To the student’s bank account

- In installments by semester

Some lenders also provide additional funding for accommodation and living expenses.

Step 4: Grace Period

Most student loans offer a grace period after graduation.

This means students don’t have to begin repayments immediately.

Typical grace periods range from:

- 6 months

- 12 months

- Until employment begins

Step 5: Repayment Begins

After the grace period ends, monthly payments start.

Repayment includes:

- Principal amount

- Interest charges

- Additional lender fees (if applicable)

The repayment period may last anywhere from 5 to 20 years.

Student Loan Interest Rates in 2026

Interest rate is one of the most important factors when choosing a student loan.

A small difference in interest rate can cost thousands over time.

Typical Student Loan Interest Rates

| Loan Type | Average Interest Rate |

|---|---|

| Government Loans | 3% – 8% |

| Private Loans | 8% – 18% |

| High-Risk Borrowers | 18%+ |

The exact rate depends on:

- Country

- Credit history

- Co-signer quality

- Loan amount

- Repayment period

- Type of institution

Fixed vs Variable Interest Rates

Fixed Interest Rate

The interest rate stays the same throughout the loan term.

Advantages

- Predictable payments

- Easier budgeting

- Protection against rising rates

Variable Interest Rate

The interest rate changes based on market conditions.

Advantages

- Lower starting rates

- Potential savings if rates fall

Risks

- Monthly payments can increase

- Long-term uncertainty

For most students, fixed-rate loans are safer and easier to manage.

Eligibility Criteria for Student Loans

Student loan requirements vary by lender, but most applicants need to meet several basic conditions.

Common Eligibility Requirements

- Admission to a recognized institution

- Valid ID or passport

- Acceptable academic performance

- Proof of family income

- Co-signer or guarantor

- Age requirements

- Citizenship or residency status

Some international student lenders may also require English proficiency scores or visa documentation.

Documents Required for Education Loans

Preparing your paperwork early improves approval chances and speeds up processing.

Commonly Required Documents

- National ID card or passport

- Admission letter

- Academic transcripts

- Fee structure from university

- Income proof of parents or guardian

- Bank statements

- Passport-size photographs

- Visa documents (for international studies)

Always double-check requirements with your lender because missing documents can delay approval.

How Much Should You Borrow?

One of the biggest student loan mistakes is borrowing more money than necessary.

Many students underestimate how difficult repayment becomes after graduation.

Smart Borrowing Rule

Only borrow what you truly need.

Focus on essential expenses such as:

- Tuition fees

- Accommodation

- Study materials

- Transportation

- Basic living costs

Avoid using student loans for:

- Luxury purchases

- Vacations

- Expensive gadgets

- Lifestyle upgrades

Remember: every extra dollar borrowed also increases future interest payments.

Benefits of Student Loans

When managed responsibly, student loans can provide life-changing opportunities.

1. Access to Higher Education

Student loans make education accessible for students who cannot afford large upfront payments.

Without financing, many talented students would never attend university.

2. Flexible Repayment Structure

Most education loans are designed with students in mind.

Repayment usually starts after graduation, giving borrowers time to secure employment.

3. Opportunity to Study Abroad

International education can be expensive.

Student loans help cover:

- Tuition

- Visa costs

- Airfare

- Accommodation

- Living expenses

This allows students to access world-class institutions and global career opportunities.

4. Building Credit History

Making on-time payments helps students establish a strong credit profile.

Good credit can help later with:

- Car financing

- Home loans

- Business funding

- Credit card approvals

Risks and Challenges of Student Loans

While student loans can be useful, they also carry serious financial responsibilities.

Understanding the risks is essential.

1. Long-Term Debt Burden

Large education loans can take many years to repay.

Some graduates struggle with debt well into adulthood.

2. Interest Accumulation

Interest keeps growing if payments are delayed or missed.

This can dramatically increase the total repayment amount.

3. Employment Uncertainty

Repayment pressure becomes difficult if graduates cannot find stable jobs quickly.

This is especially risky for students entering low-paying industries.

4. Credit Score Damage

Missing payments negatively affects credit history.

Poor credit can impact future financial opportunities.

Smart Student Loan Tips for 2026

Managing education financing wisely can save money and reduce stress.

Here are some practical strategies every student should follow.

1. Borrow Only What You Need

Avoid unnecessary debt.

Smaller loans are easier to repay and reduce interest costs.

2. Compare Multiple Lenders

Never accept the first offer without comparison.

Check:

- Interest rates

- Repayment flexibility

- Processing fees

- Grace periods

- Penalties

Even a small rate difference matters over time.

3. Prioritize Government Loans

Government-backed loans usually offer better protections and lower rates than private lenders.

Always explore public financing programs first.

4. Start Payments Early If Possible

Even small payments during study years can reduce long-term interest significantly.

This strategy lowers total loan cost.

5. Track Your Loan Regularly

Know:

- Remaining balance

- Interest rate

- Due dates

- Monthly payment amount

Ignoring your loan can lead to financial surprises later.

Best Student Loan Repayment Strategies

Repayment planning is just as important as borrowing.

The right strategy can help you become debt-free faster.

1. Standard Repayment Plan

This involves fixed monthly payments over a set period.

Benefits

- Predictable payments

- Faster loan payoff

- Lower total interest

2. Income-Based Repayment

Monthly payments depend on your earnings.

Best For

- Graduates with lower starting salaries

- Freelancers

- Self-employed professionals

This option offers flexibility during financially difficult periods.

3. Early Repayment Strategy

Paying more than the minimum reduces interest dramatically.

Even small extra payments can shorten repayment time by years.

4. Refinancing Student Loans

Some lenders allow borrowers to refinance loans at lower interest rates.

Advantages

- Lower monthly payments

- Reduced interest costs

- Simplified repayment

However, refinancing may remove certain government protections.

Scholarships vs Student Loans

Many students wonder whether scholarships are better than loans.

The reality is that both can work together.

Scholarships

Advantages

- No repayment required

- Merit-based or need-based

- Reduces financial stress

Limitations

- Highly competitive

- Limited availability

Student Loans

Advantages

- Easier access to funding

- Covers large expenses

- Flexible financing options

Limitations

- Must be repaid

- Interest charges apply

Best Strategy

The smartest approach is to combine scholarships with responsible borrowing.

This minimizes debt while still covering education costs.

Common Student Loan Mistakes to Avoid

Many borrowers create financial problems simply because they don’t understand how loans work.

Avoid these common mistakes.

1. Borrowing Excessively

Taking more money than necessary creates long-term stress.

Always calculate realistic costs.

2. Ignoring Interest Rates

A high-interest loan becomes much more expensive over time.

Always compare multiple offers before signing.

3. Missing Payments

Late payments damage your credit score and increase penalties.

Set reminders or automate payments whenever possible.

4. Not Reading Loan Terms

Many students sign agreements without understanding:

- Interest calculations

- Penalty fees

- Repayment schedules

- Grace periods

Always read the full contract carefully.

Can You Study Abroad With a Student Loan?

Yes — many lenders now specialize in international education financing.

Student loans for studying abroad can cover:

- University tuition

- Accommodation

- Visa processing

- Flight tickets

- Health insurance

- Living expenses

However, approval standards are often stricter.

Common Requirements for International Student Loans

- Strong academic performance

- Recognized university admission

- Co-signer or guarantor

- Higher financial guarantees

- Stable repayment plan

Study abroad loans are becoming increasingly common in 2026 due to growing global education demand.

Is a Student Loan Worth It?

In many cases, yes.

A student loan can provide access to education that leads to:

- Better career opportunities

- Higher earning potential

- Professional growth

- Financial independence

However, a student loan is only worth it when:

- The degree has strong career value

- Borrowing remains manageable

- Repayment planning is realistic

- The student understands the loan terms

Education financing should be viewed as a strategic investment — not free money.

Frequently Asked Questions (FAQs)

Q1: When do student loan repayments start?

Most lenders begin repayment after graduation or after a grace period of several months.

Q2: Can I get a student loan without a guarantor?

Some lenders offer no-guarantor loans, but approval is usually harder and interest rates may be higher.

Q3: Are student loan interest rates high in 2026?

It depends on the lender, country, and borrower profile. Government loans are generally cheaper than private loans.

Q4: Can I repay my student loan early?

Yes. Early repayment reduces total interest costs and helps you become debt-free faster.

Q5: What happens if I miss payments?

Missed payments can result in penalties, increased interest, and credit score damage.

Q6: Is studying abroad with a loan a good idea?

It can be worthwhile if the degree improves long-term career opportunities and earning potential.

Final Thoughts: Borrow Smart, Graduate Strong

A student loan can either become a stepping stone toward success or a financial burden that follows you for years.

The difference depends on how wisely you borrow and manage your education financing.

In 2026, students have more funding opportunities than ever before — including government loans, private education financing, and Islamic student funding solutions. But smart decision-making remains essential.

Before taking any loan:

- Compare lenders carefully

- Understand the repayment terms

- Borrow only what you truly need

- Focus on career-focused education

- Create a repayment strategy early

Education is an investment in your future, but financial responsibility matters just as much as academic success.

If you approach student loans strategically, you can achieve your educational goals while protecting your long-term financial health.